The High

For most of the game, challenger Matthew LaMagna held a large lead. During Double Jeopardy, other challenger Angela Chuang hit a Daily Double in the “I Have a Theory” category. At only ~$4000 and facing Matthew at ~$18,000, Angela had only one option: make it a true Daily Double. She did. That part was sweet.

So was the clue (paraphrasing):

Beautiful Mind John Nash is credited with launching this field in economics.

Obviously, the correct response was “What is game theory?” Angela nailed it. Again, sweet. Maybe she knows game theory!

The Low

Now the sour part. Despite her best efforts, Matthew pulled away. The scores entering Final Jeopardy were $20,800 for Matthew, $8400 for Angela, and $1200 for the returning champion. Wagers are trivial at this point. Matthew has first place locked. Angela has second place locked as well because she doubles up the third place’s dollar figure. It does not take a game theorist to see this, but it helps.

(Critically, the end dollar figures are irrelevant for second and third place. Second receives a fixed $2000; third place, $1000.)

However, despite Angela’s familiarity with game theory, she wagers $8300. The returning champion wagers nothing. Final Jeopardy’s clue is triple stumper. Angela drops to $100 and third place, when all she had to do was write $0 and guarantee herself $2000. Instead, she went home with a check for $1000.

To be fair, there might be reason to not wager $0 here even though you can guarantee second place by doing so. Everyone’s favorite love-to-hate champion Arthur Chu famously wagered enough so that he would draw with second place if second place wagered everything. But Angela wasn’t even going for that. The $8300 wager could do nothing but harm her. That was sour.

Although racing games usually do not involve much strategic interaction*, Mario Kart 8—and its dastardly item blocks—require some thinking. Over the past few months of play, I have put my on my methodological hat and found at least three topics that game theory can help sort out. Let’s get to it.

(*Of course, just about all racing games require good strategy to beat opponents—things like knowing how to cut corners, boost properly, accelerate at the start of the race, etc. Because game theory is the study of how individuals interact with each other, I am focusing on the strategically interdependent decisions—i.e., those that require me to think about what you are doing and for you to think about what I am doing.)

Mario Kart Is a Defensive Game

Here is a common but critical mistake. You race toward an item block and pick up a red shell. A split second passes by. You see a helpless opponent directly in front of you and let it loose. The red shell strikes him, and you overtake his position.

A successful maneuver? Hardly. The opponent behind you has a red shell and does the exact same thing. You explode, losing two valuable seconds. Five people pass you, including the guy you shelled. Your net gain is negative four positions.

Ready to fire? You might want to wait.

The problem here is one of externalities. When you hit someone with a shell, you benefit some. But so does everyone other than your poor victim. Thus, you only internalize a fraction of the overall benefit; most of the benefits are external to you. Meanwhile, the target internalizes every last bit of the damage.

In turn, whenever you fire off a shell, you are gambling that the small bit of benefit you internalize from striking your target exceeds the potential loss you will suffer if a shell hits you because you no longer have protection. The odds are clearly stacked against you. Hence, Mario Kart is primarily a defensive game, at least when it comes to items.

Of course, that does not mean you should always keep your shells and peels in inventory. If you are in second and have a lot of space behind you, that red shell may be your only option to reach first place. Meanwhile, when you are not in first place, keeping a shell forever is worse than dropping it before the next item block, where you will hopefully roll a mushroom or something of the sort. So you should use your items; you just need to be judicious about the timing.

On that note, the previous paragraph reveals a good time to use a red shell against an opposing Mario holding some sort of protection. If Mario is going to get rid of it, it will be right before he hits the item blocks. Anticipating this, you can time the shell just right so that Mario dumps the protection before impact.

The Item “Duel”

A “duel” in game theory is as it seems: two gunslingers have one bullet and slowly move forward until one is ready to shoot at the other. Shooting from further away has the benefit of preempting the opponent but is more inaccurate and risks allowing the other party to take a clean shot at you later. Waiting is also potentially bad because the other side might kill you first.

What to do? Modeling the dilemma produces an interesting result: both parties shoot at the same time! Yet this is perfectly reasonable if you think about it. Imagine that you were planning on shooting slightly sooner than the other party. You will hit him with some degree of probability. But if you wait just a fraction of a second longer (but before he plans to shoot you), the probability you hit him increases slightly. So you should wait. But that logic recurs infinitely. As a result, when the gunslingers behave optimally, they will shoot at the same time.

“Duels” like this have important applications, including helping to explain why two rival video game companies often release their new systems at the same time. (It also applies to competitive cycling sprints. If you have never seen this, it is very bizarre. Despite appearances, that is not slow motion instant replay.) The strategic dilemma also shows up in at least a couple situations in Mario Kart. First, imagine you are neck-and-neck for first place with an opponent and you receive the spiny shell warning. Suddenly, your incentives change. Rather than racing to first place, you should slam on the brakes and try to get into second place. That way, the shell hits him and you can move along.

Of course, your opponent has the exact same incentive. So in the split second you have to react, both of you end up pressing the brakes at the same rate, analogous to choosing to shoot at the same time. And just like a duel, sometimes you both end up dying because the explosion has such a large blast radius.

The cause of countless nightmares.

Less frequently, you might encounter a similar breaking situation around a block of items. Item blocks give better items as a player’s position increases. So if you are with a pack of four people neck-and-neck, there is a great incentive to gently press the brakes, fall back to fourth, and get three mushrooms instead of the banana peel instead. However, once again, all players have a similar incentive, resulting in the entire bunch slowing down (or at least those with the strategic wherewithal). Indeed, whoever goes into first might have a temporary advantage but will quickly fall behind due to inferior items.*

(*Item selection may be a bit trickier than what it says here. Check the comments below.)

The Game that Isn’t a Game

Finally, I want to talk about the game that isn’t strategic at all: course selection in online play. If you haven’t played online before, the system works like this. The game queues up to 12 players and randomly selects three courses. You choose one of these courses or a “random” option. After everyone has submitted their picks, the game randomly draws one player. If that player selected a course, everyone plays that track; if that player selected random, then the game randomly picks a course from the pool of all 32.

The course selection screen. Optimists like this one will soon find all their hopes and dreams crushed.

How should the course selection mechanism affect what you enter into the lottery? As it turns out, you don’t have to do any real thinking. You should just pick the track that you like the best. Unlike a traditional voting system, you don’t have to worry about what everyone else will pick. After all, if the game randomly selects your choice, then you are best off picking your favorite track; and if it chooses anyone else, then your selection is irrelevant.

If the course selection isn’t strategic in any way, then why am I talking about it? Well, as it turns out, such a mechanism that compels everyone to truthfully pick their favorite track is exceptionally rare. Economists and political scientists care about these issues greatly because effective voting mechanisms are of vital importance for both corporations and democracies. Unfortunately, the scholarly results are decidedly negative. In fact, the Gibbard-Satterthwaite theorem says that individuals will have incentive to lie about their preferences unless a person is a dictator, some options can never be chosen as the winner (i.e., we never play Mount Wario), or the selection mechanism is non-deterministic.

To see what I mean, imagine that the three tracks to select from are Music Park, Royal Raceway, and Toad’s Turnpike. (I’m going to ignore the random option for simplicity.) A majority (or plurality) of votes win. Suppose there are four other players you are squaring off against. Further, imagine that two of these guys prefer Music Park to Royal Raceway to Toad’s Turnpike; the other two prefer Royal Raceway to Toad’s Turnpike to Music Park. Meanwhile, you prefer Toad’s Turnpike to Music Park to Royal Raceway.

Is it rational for everyone to vote for his or her favorite course? No. If everyone did, we would have two votes for Music Park, two votes for Royal Raceway, and one vote for Toad’s Turnpike. With the tie between Music Park and Royal Raceway, the game might break it with a coin flip. The result is a 50% chance of Music Park and a 50% chance of Royal Raceway.

But imagine you misrepresented your preferences by voting for Music Park instead. Now Music Park has a strict majority and becomes the course that everyone will play. That is better for you than a 50% chance at Music Park and a 50% chance at Royal Raceway (your least favorite course). So you should lie! This means a majority/plurality system forces you to think about what others will select rather than just focusing on your own preferences.

While it might not be surprising that I can craft an example where you have incentive to lie, what is shocking is that just about all voting mechanisms suffer from this problem. That is the magic of the Gibbard-Satterthwaite theorem—it jumps from examples of failures to saying that just about everything will fail. The only way to break out of the problem is to give someone dictatorial powers, eliminate some choices from winning under any circumstance, or have the voting mechanism choose non-deterministically. Nintendo’s selection system opts for the last resolution.

In sum, just pick what you want on the course selection screen. And thanks to the incentive to tell the truth, let me tabulate all of your selections to investigate the world’s favorite courses.

Last week’s episode of The Good Wife (““Trust Issues”) was interesting for two reasons: it used a “ripped from the headlines” legal case that I discuss in my book on bargaining and the legal argument they use is essentially a trivial application of pre-play cheap talk in a repeated prisoner’s dilemma.

The $9 Billion Google/Apple Anti-Trust Lawsuit

First, the background of the real life version of the case. In the early 2000s, Google and Apple (along with Adobe and Intel) allegedly had a “no poaching” gentleman’s agreement. That is, each company in the group pledged to not attempt to hire employees at any of the other companies. The employees eventually figured out what was going on, filed a $9 billion lawsuit, and settled in April 2014 for an undisclosed amount.

Why is the practice illegal? It goes without saying that quashing competition among firms hurts the employees’ bargaining power, and the law is there to protect those employees. But what is not so clear is just how attractive a no poaching agreement is to the firms. In fact, when companies play by the rules, just about all of the potential for profit goes into the employees’ hands.

To see why, imagine that Google and Apple both wanted to hire Karen. Karen has impressive computer programming skills. And because Google and Apple value computing skills at a roughly equal rate, suppose that the most Google would be willing to pay her is $200,000 while Apple’s maximum is $195,000. Put differently, $200,000 and $195,000 represent the break even points for the respective companies. Put differently again, Karen will bring in $200,000 in profits to Google and $195,000 to Apple, so hiring her for any more than that will result in a net loss.

How will that profit ultimately be divided between Karen and her employer? You might think that Google should be the one hiring her. And you are right—she is worth $5000 more to Google than Apple. You might also think that Google will profit handsomely from her employment. However, as I discuss at length in the book, the logic of bargaining shows this to be untrue. If Google offers Karen any less than $195,000, she can always secure a job from Apple; this is because Apple values her at that amount, and so Apple would be willing to slightly outbid Google to hire her. Thus, the outbidding process ultimately ensures that Karen receives at least $195,000. She is the real winner. Although Google might still profit from her employment, its net gain will not exceed $5000 ($200,000 – $195,000).

Negotiating Collusion

So the firms have great incentive to collude, drive down wages, and secure more of the profits for themselves. What does that sort of collusion look like?

Well, we might think of it as a repeated prisoner’s dilemma. In this type of interaction, in any given year, each of us would maximize profits by trying to poach the rival firm’s employees regardless of what the other firm chooses to do. (If you don’t poach, then I make out like a bandit. If you do poach, I’m still better off poaching and not losing all the employees.) However, because each of us is poaching and driving up employee wages, both us are ultimately worse off than if we could enforce an agreement that required us to cooperate with each other and not poach.

Of course, anti-trust laws prevent us from explicitly contracting such an agreement in a legally enforceable manner. However, an informal and internally enforceable agreement is possible. Suppose we both start off by cooperating with each other by not poaching. Then, in each subsequent year, if both of us have consistently cooperated before, we continue cooperating. Otherwise, we revert to poaching.

Would anyone like to break the agreement? No. Although I could gain a temporary advantage against you by poaching your employees today, the higher wages over the long-term with mutual poaching are going to vastly outstrip that short-term benefit.

This is exactly the type of agreement Google and Apple struck. In fact, when a Google recruiter attempted to hire some Apple employees, Steve Jobs shot the following email to Google bigwigs: “If you hire a single one of these people, that means war.”

Alicia Florrick’s Defense

The episode of The Good Wife featured fictionalized versions of Google and Apple involved in the same affair. Like reality, employees caught on and sued.

The plaintiff’s lawyers thought they had the case in the bag. Indeed, they had turned one of the owners of a trust company against the defense. He went on record that the defense had negotiated the terms of the no poaching policy explicitly and was very happy to agree to the deal.

Alicia Florrick (the defense attorney and titular Good Wife) had a great defense: any discussion of such an agreement is not an unambiguous signal of plans to break the law. These repeated prisoner’s dilemmas have an interesting property in that regardless of whether you plan to cooperate with the other company or screw them over at the first possible moment, you always want to convince the other side that you will cooperate. If you plan to cooperate, then you want to tell the other side to cooperate as well so you can sustain that cooperation in the long term. If you want to follow the law and poach freely instead, you still want to convince the other side that you are going to cooperate so that they cooperate as well, allowing you to screw them over in the process.

So Florrick points out that this type of pre-play communication is meaningless. Regardless of the ultimate intend, the defendant would say the exact same thing. The testimony therefore proves nothing. The plaintiff promptly settled.

All told, I really appreciate two things about the episode: its sophisticated understanding of a potentially very complicated strategic situation and the how punny the “Trust Issues” title is.

McDonald’s Monopoly begins again today. With that in mind, I thought I would update my explanation of the game theory behind the value of each piece, especially since my new book on bargaining connects the same mechanism to the De Beers diamond monopoly, star free agent athletes, and a shady business deal between Google and Apple. Here’s the post, mostly in its original form:

__________________________________

McDonald’s Monopoly is back. As always, if you collect Park Place and Boardwalk, you win a million dollars. I just got a Park Place. That’s worth about $500,000, right?

Actually, it is worth nothing. Not close to nothing, but absolutely, positively nothing.

It helps to know how McDonald’s structures the game. Despite the apparent value of Park Place, McDonald’s floods the market with Park Place pieces, probably to trick naive players into thinking they are close to riches. I do not have an exact number, but I would imagine there are easily tens of thousands of Park Places floating around. However, they only one or two Boardwalks available. (Again, I do not know the exact number, but it is equal to the number of million dollar prizes McDonald’s want to give out.)

Even with that disparity, you might think Park Place maintains some value. Yet, it is easy to show that this intuition is wrong. Imagine you have a Boardwalk piece and you corral two Park Place holders into a room. (This works if you gathered thousands of them as well, but you only need two of them for this to work.) You tell them that you are looking to buy a Park Place piece. Each of them must write their sell price on a piece of paper. You will complete the transaction at the lowest price. For example, if one person wrote $500,000 and the other wrote $400,000, you would buy it from the second at $400,000.

Assume that sell prices are continuous and weakly positive, and that ties are broken by coin flip. How much should you expect to pay?

The answer is $0.

The proof is extremely simple. It is clear that both bidding $0 is a Nash equilibrium. (Check out my textbook or watch my YouTube videos if you do not know what a Nash equilibrium is.) If either Park Place owner deviates to a positive amount, that deviator would lose, since the other guy is bidding 0. So neither player can profitably deviate. Thus, both bidding 0 is a Nash equilibrium.

What if one bid $x greater than or equal to 0 and the other bid $y > x? Then the person bidding y could profitably deviate to any amount between y and x. He still wins the piece, but he pays less for it. Thus, this is a profitable deviation and bids x and y are not an equilibrium.

The final case is when both players bid the same amount z > 0. In expectation, both earn z/2. Regardless of the tiebreaking mechanism, one player must lose at least half the time. That player can profitably deviate to 3z/8 and win outright. This sell price is larger than the expectation.

This exhausts all possibilities. So both bidding $0 is the unique Nash equilibrium. Despite requiring another piece, your Boardwalk is worth a full million dollars.

What is going wrong for the Park Place holders? Supply simply outstrips demand. Any person with a Park Place but no Boardwalk walks away with nothing, which ultimately drives down the price of Park Place down to nothing as well.

Moral of the story: Don’t get excited if you get a Park Place piece.

Note 1: If money is discrete down to the cent, then the winning bid could be $0 or $0.01. (With the right tie breaker, it could also be $0.02.) Either way, this is not good for owners of Park Place.

Note 2: In practice, we might see Park Place sell for some marginally higher value. That is because it is (slightly) costly for a Boardwalk owner to seek out and solicit bids from more Park Place holders. However, Park Place itself is not creating any value here—it’s purely the transaction cost.

Note 3: An enterprising Park Place owner could purchase all other Park Place pieces and destroy them. This would force the Boardwalk controller to split the million dollars. While that is reasonable to do when there are only two individuals like the example, good luck buying all Park Places in reality. (Transaction costs strike again!)

__________________________________

Now time for an update. What might not have been clear in the original post is that McDonald’s Monopoly is a simple illustration of a matching problem. Whenever you have a situation with n individuals who need one of m partners, all of the economic benefits go to the partners if m < n. The logic is the same as above. If an individual does not obtain a partner, he receives no profit. This makes him desperate to partner with someone, even if it means drastically dropping his share of the money to be made. But then the underbidding process begins until the m partners are taking all of the revenues for themselves.

In the book, I have a more practical example involving star free agent athletes. For example, there is only one LeBron James. Every team would like to sign him to improve their chances of winning. Yet this ultimately results in the final contract price to be so high that the team doesn’t actually benefit much (or at all) from signing James.

Well, that’s how it would work if professional sports organizations were not scheming to stop this. The NBA in particular has a maximum salary. So even if LeBron James is worth $50 million per season, he won’t be paid that much. (The exact amount a player can earn is complicated.) This ensures that the team that signs him will benefit from the transaction but takes money away from James.

Non-sports business scheme in similar ways. More than 100 year ago, the De Beers diamond company realized that new mine discoveries would mean that diamond supply would soon outstrip demand. This would kill diamond prices. So De Beers began purchasing tons of mines to intentionally limit production and increase price. Similarly, Apple and Google once had a “no compete” informal agreement to not poach each other’s employees. Without the outside bidder, a superstar computer engineer would not be able to increase his wage to the fair market value. Of course, this is highly illegal. Employees filed a $9 billion anti-trust lawsuit when they learned of this. The parties eventually settled the suit outside of court for an undisclosed amount.

To sum up, matching is good for those in demand and bad for those in high supply. With that in mind, good luck finding that Boardwalk!

A common question I get is what game theory tells us about negotiating a pay raise. Because I just published a book on bargaining, this is something I have been thinking about a lot recently. Fortunately, I can narrow the fundamentals to three simple points:

1) Virtually all of the work is done before you sit down at the table.

When you ask the average person how they negotiated their previous raise, you will commonly hear anecdotes about how that individual said some (allegedly) cunning things, (allegedly) outwitted his or her boss, and received a hefty pay hike. Drawing inferences from this is problematic for a number of reasons:

Anecdotal “evidence” isn’t evidence.

The reason for the raise might have been orthogonal to what was said.

Worse, the raise might have been despite what was said.

It assumes that the boss is more concerned about dazzling words than money, his own job performance, and institutional constraints.

The fourth point is especially concerning. Think about the people who control your salaries. They did not get their job because they are easily persuaded by rehearsed speeches. No, they are there because they are good at making smart hiring decisions and keeping salaries low. Moreover, because this is their job, they engage in this sort of bargaining frequently. It would thus be very strange for someone like that to make such a rookie mistake.

So if you think you can just be clever at the bargaining table, you are going to have a bad time. Indeed, the bargaining table is not a game of chess. It should simply be a declaration of checkmate. The real work is building your bargaining leverage ahead of time.

2) Do not be afraid to reject offers and make counteroffers.

Imagine a world where only one negotiator had the ability to make an offer, while the other could only accept or reject that proposal. Accepting implements the deal; rejecting means that neither party enjoys the benefits of mutual cooperation. What portion of the economic benefits will the proposer take? And how much of the benefits will go to the receiver?

You might guess that the proposer has the advantage here. And you’d be right. What surprises most people, however, is the extent of the advantage: the proposer reaps virtually all of the benefits of the relationship, while the receiver is barely any better off than had the parties not struck a deal.

How do we know this? Game theory allows us to study this exact scenario rigorously. Indeed, the setup has a specific name: the ultimatum game. It shows that a party with the exclusive right to make proposals has all of the bargaining power.

That might seem like a big problem if you are the one receiving the offers. Fortunately, the problem is easy to solve in practice. Few real life bargaining situations expressly prohibit parties from making counteroffers. (As I discuss in the book, return of security deposits is one such exception, and we all know that turns out poorly for the renter—i.e., the receiver of the offer.) Even the ability to make a single counteroffer drastically increases an individual’s bargaining power. And if the parties could potentially bargain back and forth without end—called Rubinstein bargaining, perhaps the most realistic of proposal structures—bargaining equitably divides the benefits.

As the section header says, the lesson here is that you should not be afraid to reject low offers and propose a more favorable division. Yet people often fail to do this. This is especially common at the time of hire. After culling through all of the applications, a hiring manager might propose a wage. The new employee, deathly afraid of losing the position, meekly accepts.

Of course, the new employee is not fully appreciating the company’s incentives. By making the proposal, the company has signaled that the individual is the best available candidate. This inevitably gives him a little bit of wiggle room with his wage. He should exercise this leverage and push for a little more—especially because starting wage is often the point of departure for all future raise negotiations.

3) Increase your value to other companies.

Your company does not pay you a lot of money to be nice to you. It pays you because it has no other choice. Although many things can force a company’s hand in this manner, competing offers is particularly important.

Imagine that your company values your work at $50 per hour. If you can only work for them, due the back-and-forth logic from above, we might imagine that your wage will land in the neighborhood of $40 per hour. However, suppose that a second company exists that is willing to pay you up to $25 per hour. Now how much will you make?

The answer is no less than $40 per hour. Why? Well, suppose not. If your current company is only paying you, say, $30 per hour, you could go to the other company and ask for a little bit more. They would be obliged to pay you that since they value you up to $40 per hour. But, of course, your original company values you up to $50 per hour. So they have incentive to ultimately outbid the other company and keep you under their roof.

Game theorists call such alternatives “outside options”; the better your outside options are, the more attractive the offers your bargaining partner has to make to keep you around. Consequently, being attractive to other companies can get you a raise with your current company even if you have no serious intention to leave. Rather, you can diplomatically point out to your boss that a person with your particular skill set typically makes $X per year and that your wage should be commensurate with that amount. Your boss will see this as a thinly veiled threat that you might leave the company. Still, if the company values your work, she will have no choice but to bump you to that level. And if she doesn’t…well, you are valuable to other companies, so you can go make that amount of money elsewhere.

Conclusion

Bargaining can be a scary process. Unfortunately, this fear blinds us to some of the critical facets of the process. Negotiations are strategic; only thinking about your worries and concerns means you are ignoring your employer’s worries and concerns. Yet you can use those opposing worries and concerns to coerce a better deal for yourself. Employers do not hold all of the power. Once you realize this, you can take advantage of the opposing weakness at the bargaining table.

I talk about all of these issues in greater length in my book, Game Theory 101: Bargaining. I also cover a bunch of real world applications to these and a whole bunch of other theories. If this stuff seems interesting to you, you should check it out!

We argue that formal theory and historical case studies, in particular those that use process-tracing, are extremely well-suited companions in multi-method research. To bolster future research employing both case studies and formal theory, we suggest some best practices as well as some (common) pitfalls to avoid.

Since the research note is short by nature, I won’t spend too much extra space discussing it here. You’d be better off skimming or reading the note itself. In essence, though, we argue that formal theory and case studies are natural methodological allies. We also advocate for serious interpretation of a model’s cutpoint into the informal analysis. Manuscripts that combine formal theory with case studies too often spend considerable time developing the model only to ignore it when they begin discussing substance. They should be tied together.

Also, and something that I stress heavily in my book project on nuclear proliferation, we must be very careful in how we interpret those cutpoints. For example, a common fallacy takes the following form: the model says w occurs if x > y + z. The case study then goes to great lengths to prove that y was close to 0 or negative, therefore w should occur. This overlooks the values of x and z, however—even with y equal to 0, the inequality could still fail depending on the relationship between the other parameters. Put differently, and with certain notable exceptions detailed in the research note, we must think about the cutpoints holistically.

Tesla Motors recently announced that it is opening its electric car patents to competitors. The buzz around the Internet is that this is another case of Tesla’s CEO Elon Musk doing something good for humanity. However, the evidence suggests another explanation: Tesla is doing this to make money, and that’s not a bad thing.

The issue Tesla faces is what game theorists call a coordination problem. Specifically, it is a stag hunt:

For those unfamiliar and who did not watch the video, a stag hunt is the general name for a game where both parties want to coordinate on taking the same action because it gives each side its individually best outcome. However, a party’s worst possible outcome is to take that action while the other side does not. This leads to two reasonable outcomes: both coordinate on the good action and do very well or both do not take that action (because they expect the other one not to) and do poorly.

This is a common problem in emerging markets. The core issue is that some technologies need other technologies to function properly. That is, technology A is worthless without technology B, and technology B is worthless without technology A. Manufacturers of A might want to produce A and manufacturers of B might want to produce B, but they cannot do this profitably without each other’s support.

Take HDTV as a recent example. We are all happy to live in a world of HD: producers now create a better product, and consumers find the images to be far more visually appeasing. However, the development of HDTV took longer than it should have. The problem was that producers had no reason to switch over to HD broadcasting until people owned HDTVs. Yet television manufacturers had no reason to create HDTVs until there were HD programs available for consumption. This created an awkward coordination problem in which both producers and manufacturers were waiting around for each other. HDTV only became commonplace after cheaper production costs made the transition less risky for either party.

I imagine car manufacturers faced a similar problem a century ago. Ford and General Motors may have been ready to sell cars to the public, but the public had little reason to buy them without gas stations all around to make it easy to refuel their vehicles. But small business owners had little reason to start up gas stations without a large group of car owners around to purchase from them.

The above problem should make Tesla’s major barrier clear. Tesla has the electric car technology ready. What they lack is a network of charging stations that can make long-distance travel with electric cars practical. Giving away the patents to competitors potentially means more electric cars on the road and more charging stations, without having to spend significant capital that the small company does not have. Tesla ultimately wins because they have a first-mover advantage in developing the technology.

So this is less about altruism and more about self-interest. But that is not a bad thing. 99% of the driving force behind economics is mutual gain. I think this fact gets lost in the modern political/economic debate because there are some (really bad) cases where that is not true. But here, Tesla wins, other car manufacturers win, and consumers win.

Oh, oil producing companies lose. Whatever.

H/T to Dillon Bowman (a student of mine at the University of Rochester) and /u/Mubarmi for inspiring this post.

With the World Cup starting today, now is a great time to discuss the game theory behind soccer penalty kicks. This blog post will do three things: (1) show that penalty kicks is a very common type of game and one that game theory can solve very easily, (2) players behave more or less as game theory would predict, and (3) a striker becoming more accurate to one side makes him less likely to kick to that side. Why? Read on.

The Basics: Matching Pennies

Penalty kicks are straightforward. A striker lines up with the ball in front of him. He runs forwards and kicks the ball toward the net. The goalie tries to stop it.

Despite the ordering I just listed, the players essentially move simultaneously. Although the goalie dives after the striker has kicked the ball, he cannot actually wait to the ball comes off the foot to decide which way to dive—because the ball moves so fast, it will already be behind him by the time he finishes his dive. So the goalie must pick his strategy before observing any relevant information from the striker.

This type of game is actually very common. Both players pick a side. One player wants to match sides (the goalie), while the other wants to mismatch (the striker). That is, from the striker’s perspective, the goalie wants to dive left when the striker kicks left and dive right when the striker kicks right; the striker wants to kick left when the goalie dives right and kick right when the goalie dives left. This is like a baseball batter trying to guess what pitch the pitcher will throw while the pitcher tries to confuse the batter. Similarly, a basketball shooter wants a defender to break the wrong way to give him an open lane to the basket, while the defender wants to stay lined up with the ball handler.

Because the game is so common, it should not be surprised that game theorists have studied this type of game at length. (Game theory, after all, is the mathematical study of strategy.) The common name for the game is matching pennies. When the sides are equally powerful, the solution is very simple:

If you skipped the video, the solution is for both players to pick each side with equal probability. For penalty kicks, that means the striker kicks left half the time and right half the time; the goalie dives left half the time and dives right half the time.

Why are these optimal strategies? The answer is simple: neither party can be exploited under these circumstances. This might be easier to see by looking at why all other strategies are not optimal. If the striker kicked left 100% of the time, it would be very easy for the goalie to stop the shot—he would simply dive left 100% of the time. In essence, the striker’s predictability allows the goalie to exploit him. This is also true if the striker is aiming left 99% of the time, or 98% of the time, and so forth—the goalie would still want to always dive left, and the striker would not perform as well as he could by randomizing in a less predictable manner.

In contrast, if the striker is kicking left half the time and kicking right half the time, it does not matter which direction the goalie dives—he is equally likely to stop the ball at that point. Likewise, if the goalie is diving left half the time and diving right half the time, it does not matter which direction he striker kicks—he is equally likely to score at that point.

The key takeaways here are twofold: (1) you have to randomize to not be exploited and (2) you need to think of your opponent’s strategic constraints when choosing your move.

Real Life Penalty Kicks

So that’s the basic theory of penalty kicks. How does it play out in reality?

How did they figure this out? To begin, they used a more sophisticated model than the one I introduced above. Real life penalty kicks differ in two key ways. First, kicking to the left is not the same thing as kicking to the right. A right-footed striker naturally hits the ball harder and more accurately to the left than the right. This means that a ball aimed to the right is more likely to miss the goal completely and more likely to be stopped if the goalie also dives that way. And second, a third strategy for both players is also reasonable: aim to the middle/defend the middle.

Regardless of the additional complications, there are a couple of key generalizations that hold from the logic of the first section. First, a striker’s probability of scoring should be equal regardless of whether he kicks left, straight, or right. Why? Suppose this were not true. Then someone is being unnecessarily exploited in this situation. For example, imagine that strikers are kicking very frequently to the left. Realizing this, goalies are also diving very frequently to the left. This leaves the striker with a small scoring percentage to the left and a much higher scoring percentage when he aims to the undefended right. Thus, the striker should be correcting his strategy by aiming right more frequently. So if everyone is playing optimally, his scoring percentage needs to be equal across all his strategies, otherwise some sort of exploitation is available.

Second, a goalie’s probability of not being scored against must be equal across all of his defending strategies. This follows from the same reason as above: if diving toward one side is less likely to result in a goal, then someone is being exploited who should not be.

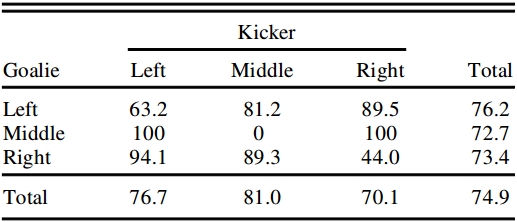

All told, this means that we should observe equal probabilities among all strategies. And, sure enough, this is more or less what goes on. Here’s Figure 4 from the article, which gives the percentage of shots that go in for any combination of strategies:

The key places to look are the “total” column and row. The total column for the goalie on the right shows that he is very close to giving up a goal 75% of the time regardless of his strategy. The total row for the striker at the bottom shows more variance—in the data, he scores 81% of the time aiming toward the middle but only 70.1% of the time aiming to the right—but those differences are not statistically significant. In other words, we would expect that sort of variation to occur purely due to chance.

Thus, as far as we can tell, the players are playing optimal strategies as we would suspect. (Take that, you damn dirty apes!)

Relying on Your Weakness

One thing I glossed over in the second part is specifically how a striker’s strategy should change due to the weakness of the right side versus the left. Let’s take care of that now.

Imagine you are a striker with an amazingly accurate left side but a very inaccurate right side. More concretely, you will always hit the target if you shoot left, but you will miss some percentage of the time on the right side. Realizing your weakness, you spend months practicing your right shot and double its accuracy. Now that you have a stronger right side, how will this affect your penalty kick strategy?

The intuitive answer is that it should make you shoot more frequently toward the right—after all, your shot has improved on that side. However, this intuition is not always correct—you may end up shooting less often to the right. Equivalently, this means the more inaccurate you are to one side, the more you end up aiming in that direction.

Why is this the case? If you want the full explanation, watch the following two videos:

The shorter explanation is as follows. As mentioned at the end of the first section of this blog post, players must consider their opponent’s capabilities as they develop their strategies. When you improve your accuracy to the right side, your opponent reacts by defending the right side more—he can no longer so strongly rely on your inaccuracy as a phantom defense. So if you start aiming more frequently to the right side, you end up with an over-correction—you are kicking too frequently toward a better defended side. Thus, you end up kicking more frequently to the left to account for the goalie wanting to dive right more frequently.

“Chimps Outsmart Humans When It Comes To Game Theory” has been making the social media rounds today. Unfortunately, this seems to be a case of social media run amok–the paper has some interesting results, but that interpretation is horribly off base.

Below, I will give four reasons why we shouldn’t conclude that chimps are better at game theory than humans. But first, let’s quickly review what happened. A bunch of chimps, Japanese students, and villagers played some basic, zero-sum, simultaneous move games like matching pennies. The mixed strategy algorithm derives equilibrium predictions of what each player should do under these scenarios. As it turns out, chimps played strategies closer to the equilibrium predictions. Therefore, the proposed conclusion is that chimps are better game theorists than humans.

So what’s wrong here? Well…

The Sample Size Is Lacking

Who participated in the study? Six chimps, thirteen female Japanese students, and twelve males from Guinea. We can’t generalize differences between these groups in a meaningful way without a larger sample size.

The Chimps Aren’t a Random Sample

From the study:

Six chimpanzees (Pan Troglodytes) at the Kyoto University Primate Research Institute voluntarily participated in the experiment. Each chimpanzee pair was a mother and her offspring…all six had previously participated in cognitive studies, including social tasks involving food and token sharing.

There are a couple of problems here. First, the pairs of chimps that played are related. It stands to reason that a mother who is good at these games would produce offspring that is also good at these games. So we really aren’t looking at six chimps so much as three. Ouch.

(It should be noted that the Japanese students aren’t really random either since they all come from the same university. However, this is true for many studies of this sort, so I’m going to overlook it.)

Second, these aren’t even your regular chimps. They have played plenty of games before!

Combined, this is like taking a group of University of Rochester Department of Political Scientist (URDPS) students and comparing their results to a group of random Californians. The URDPS group is “related” (they all go to the same school) and they all have plenty of experience playing games (at least three semesters’ worth). They would undoubtedly play more rationally than the random group from California. But you can’t use this to claim that New Yorkers play more rationally than Californians. Yet you are seeing the analogous claim being made.

They Aren’t Playing the Game the Researchers Are Testing Against

Only the researchers knew the game that the players were playing. In contrast, the players only knew their payoffs, not their opponents’. The mixed strategy algorithm only makes predictions about how players should play given that all facets of the game are common knowledge. That’s clearly not the case here.

Instead, the real game here is spending a number of iterations of the game trying decipher what your opponent’s payoffs are and then figuring out how to strategize accordingly. It’s not clear how to interpret the results in this light, though it is interesting that the (small, biased sample of) chimps figured this out more quickly.

The Game Was Not Inter-species

If you want to say that chimps are better at these games than humans, you need to have chimps playing humans. You would then have them play some number of iteration and see who received more apples/yen by the end of the game. Instead, it was chimps versus chimps and humans against humans. With that data, you cannot claim one party is better than the other.

Nash Equilibrium Isn’t a Good Baseline

“Fine,” you might say in response to the last point, “but the chimps still played closer to the Nash equilibrium strategies than humans. Therefore, chimps are better game theorists than humans are.” That’s still not want we want to know, though. Who cares if the players were playing Nash? If I played this game tomorrow, would I play Nash? Yes–if I thought the other player was clever enough to do the same. If not, I would try to beat them.

This is a nuanced problem, so let’s look at an example. If you ask people about soccer penalty kicks, they will likely tell you that you should kick more frequently to your stronger side as it becomes more and more accurate. This is wrong: you should increase your reliance on your weaker side. Knowing this, if I played the role of the goalie, I would start diving to the kicker’s stronger side more frequently. The kicker would do poorly and I would do very well.

How would the study interpret this? It would say that we are both bad at game theory! But that’s not what’s going on here. We have one bad strategist and one sophisticated one. The interpretation of the study would get half of it right but completely blow the other half. Worse, a sophisticated goalie taking advantage of the kicker’s incompetence would outperform a goalie who played Nash instead.

Nash equilibrium is useful for many reasons; testing whether one species is better than another with it as a baseline is not one of them.

I’d have to go through the paper more closely than I have so far to give an overall impression of it. However, even without that, it is clear that the way social media is describing the results is very questionable.

Every now and then, I hear someone say that game theory doesn’t tell us anything we don’t already know. In a sense, they are right—game theory is a methodology, so it’s not really telling us anything that our assumptions are not. However, I challenge someone to tell me that they would have believed most of the things below if we didn’t have formal modeling.

People often take aggressive postures that lead to mutually bad outcomes even though mutual cooperation is mutually preferable. Source.

Even if everyone agrees that an outcome is everyone’s favorite, they might not get that outcome. Source.

Sometimes having fewer options is better than having more options. Source.

On a penalty kick, soccer players might wish to kick more frequently toward their weaker side as their weaker side becomes increasingly inaccurate. Source.

In a duel, both gunslingers should shoot at the same time, even if one is a worse shot and would seem to benefit by walking closer to his target. Source.

There’s a reason why gas stations are on the same corner and politicians adopt very similar platforms. And it’s the same reason. Source.

Closing roads can improve everyone’s commute time. Source.

Fewer witnesses to a crime might be preferable to more. Source.

You should bid how much you value the good at stake in a second price auction. Source.

If you pay the value you think something is worth, you are going to end up with a negative net profit. Source.

Lighting money on fire is often profitable. Source.

Going to college can be valuable even if college doesn’t teach you anything. Source.

An animal might be better off jumping high in the air repeatedly than running away from a predator. Source.

Knowing just slightly more about the value of your car than a potential buyer can make it impossible to sell it. Source.

Nigerian email scammers should say they are from Nigeria even though just about everyone is familiar with the scam. Source.

Everyone might mimic everyone else just because two people chose to do the same thing. Source.

A biased media may be better than an unbiased media. Source.